Skewness

Loading…

Loading…

Kurtosis

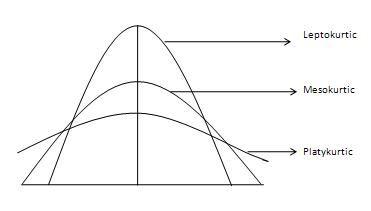

The degree of tailedness of a distribution is measured by kurtosis. It tells us the extent to which the distribution is more or less outlier-prone (heavier or light-tailed) than the normal distribution. Three different types of curves, courtesy of Investopedia, are shown as follows −

It is difficult to discern different types of kurtosis from the density plots (left panel) because the tails are close to zero for all distributions. But differences in the tails are easy to see in the normal quantile-quantile plots (right panel).

The normal curve is called Mesokurtic curve. If the curve of a distribution is more outlier prone (or heavier-tailed) than a normal or mesokurtic curve then it is referred to as a Leptokurtic curve. If a curve is less outlier prone (or lighter-tailed) than a normal curve, it is called as a platykurtic curve. Kurtosis is measured by moments and is given by the following formula −

Loading…